Cost of living up, interest rates up, financial difficulties up. What can be done now?

“Rising inflation”, “Cost of living pressures”, “Escalating Interest rates”, “Looming credit crunch due to failing regional banks.”…

It seems that in the last few months, business and economic news channels around the world have had more and more to report on these headwinds that are facing us all. Fueled by a hefty post-lockdown bill, global supply chain constraints, a slow recovery to productivity and a far-reaching war in Ukraine, today’s implications are no overnight surprise, but there are few in the western world looking forward to the need to tighten belts in the next few months and possibly years. There are some emerging, green shoots of hope, however, and as even the most amateur economists understand – upturns DO follow downturns. But most of us also live in the world of today – how long will it be before these effects that have built up over the last year or so fade from our day to day concerns?

For retailers, and notwithstanding the hopeful outlook for tomorrow, these financial realities impact their operations NOW – in terms of revenue, costs and access to working capital – and often have serious implications. For some, an inability to manage those implications presents a real and sometimes existential threat and retailers must look to all areas of their business for help. The best retailers have always seen store automation, operational efficiency, process optimization and working capital improvements as tools to improve their business, and a perhaps unlikely and sometimes overlooked area – that of physical cash management – can deliver benefits in each of these dimensions. For cash-accepting physical retailers and merchants potentially huge gains can be realized through considered application of Cash Managed Services and Cash Automation Technology.

How do these pressures affect retailers?

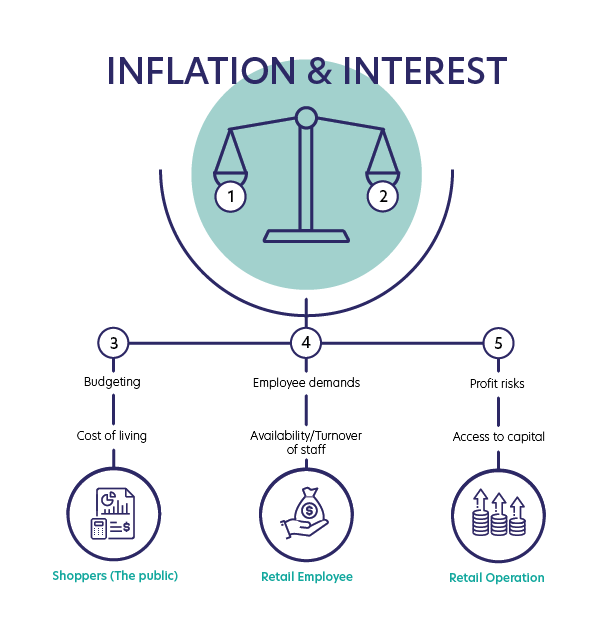

The 5 points of the inflation and interest burden on retail

- As at June 2023, inflation in the USA is still at over twice the Federal Reserve target rate, and UK and Eurozone rates remain high at 8.7% and 6.1% respectively. As we all know, high inflation drives up the cost of living for consumers, putting pressure on our ability to spend. These same increased costs and others in the retail operation (energy, fuel, cost of goods etc) that cannot be passed on to consumers as price increases result in profit squeezes for retailers.

- To control inflation, central banks raise base interest rates. As those rates go up, costs of borrowing are driven upwards – again, affecting both consumers and retailers. For consumers, this affects those with mortgages and loans, further pressurizing disposable income and retail spending – a “double whammy” for most consumers. For retailers, access to business as usual working capital, investment loans for business growth, range expansion, store refurbishments and other operational improvements becomes more expensive and sometimes more restricted.

- Both trends of inflation and interest rates put pressure on consumers’ disposable income, thus reducing retail turnover in most segments. This is, of course, bad but not surprising news. What may be less obvious is that when times are hard, consumers tend to look to techniques for better budgeting. The UK’s Nationwide Building Society reported a 19% increase in ATM Cash Withdrawals in 2022 over 2021 as consumers responded to the cost of living crisis. Earlier this year, research showed that around 50% of respondents in the USA used more cash now than a year ago citing that digital ways of paying made them spend more than they had intended (Fortune/Credit Karma). A trend that one might attribute to the less tech-savvy generations, or the less affluent “unbanked” and “underbanked” but in truth, switching to cash as a budgeting vehicle has been observed across most demographic groups.

- The other outlet for these two pressures of price uplifts and borrowing cost increases is that demand for higher salaries also increases, and in retail this is no exception. Retail is highly dependent on people and their salaries are rising – the cost of “employing humans” is going up. This is on top of a pre-lockdown upward push on minimum wages in many countries, as well as a post-lockdown and furlough trend that already put a squeeze on retail staff availability (In April 2022, there were 11.4m vacancies in retail in the USA – a 59% increase compared to pre-pandemic levels according to the US Bureau of Labor). Many people are simply not prepared to take income risks again by working in what they perceive as a volatile retail industry. Those that remain in the retail industry now command higher salaries, and also make other demands to “de-stress” themselves in those jobs, eg avoiding cash handling, and personal risk in general.

- These factors add cost and revenue risk into the retail operation while continued access to capital (for inventory, new product lines, store refits and expansions) is still a big consideration for successful retail survival and growth. This risk to the retail operation drives up the cost of capital and its availability down. Although the US Federal Fund Rate is an eye-watering 5.25% compared to 0.25% just over a year ago, the current prime rate for low risk borrowing stands at 8.25%. European and UK lending rate trends have been largely the same. The prime rate is the least risky lending rate and is typically offered to other banks and extremely wealthy individuals with outstanding creditworthiness. Retail is not a low risk business, and as such, most constituents are required to pay higher than Prime Rates for borrowing. Not surprisingly, the sector has seen much fluctuation in the last few years with major brands going out of business, or otherwise disappointing their creditors. According to cbinsights.com, there were 22 and 41 major USA retail bankruptcies in 2019 and 2020 respectively – doubtlessly impacted by Covid and lockdown actions. Despite a return to “normal” levels of bankruptcies in the last two years, already by the mid-point of June 2023 we’re tracking to be at these same Covid levels of bankruptcies again – this time attributed to the cost of living pressures. Many times, retailers are not seen by banks as “safe” businesses and current market conditions add to risk and therefore lending rates. Retailers may experience borrowing rates well in excess of 10-12% adding further pressure and cost to the retail operation, and in some cases, restricting access to capital to catastrophic levels.

Unfortunately, this seems to present a very bleak picture, but we can see signs of a turnaround, and the situation may be one which is over in months rather than years! Indeed, June 2023’s reports from the US Federal Government show a marked reduction in inflation rates from a year ago, and consensus is that these rates are on their way down. In business, of course, timing, survival and NOW are everything, and NOW may be the right time to look at or revisit a Cash Automation strategy for the retail business.

Retailers may experience borrowing rates well in excess of 10-12% adding further pressure and cost to the retail operation, and in some cases, restricting access to capital to catastrophic levels.

So, what are Cash Automation and Cash Managed Service, and how can these things help ?

Simply, Cash Automation is a portfolio of technology that allows a retail store to collect, validate, count and secure its cash revenues, ready for collection or deposit to the bank. Cash is deposited through a Bill Validator (that identifies and authenticates each note) and stored in a secure safe, and the device is typically referred to as a Smart Safe. Advanced forms of this technology can also “recycle” this cash – in other words, dispense the cash for particular applications: for example, dispensing change at point of sale/point of service stations; issuing floats to tills; cashing cheques for customers; paying suppliers and so on.

A Cash Managed Service goes a step further and is the outsourced service that provides and manages this technology for the retailer, essentially providing a cash service in the store. It has the added benefits that the management of cash pickup, change delivery, reconciliation and so on are all provided as part of a regular subscription. For a monthly fee, in-store end to end cash management is provided for the retailer by a cash management solution provider. In many cases, the Managed Service Provider will agree to own the cash in the Cash Automation Device and credit the day’s takings at the end of each day to the retailer – while the cash physically remains in the store. This is enabled through the Managed Service Provider’s trust in the device and environment (and therefore the cash balance in the device) being absolute.

This has clear benefits when, as is the case today, cash takings are increasing, employee costs are rising and access to cheap working capital is shrinking. Cash Automation can help improve the situation in all three of these areas.

As cash revenue increases, so too can cash processing costs, in a manual world. Without automation, more frequent counting, till lifts, storage, banking processes should be expected. Manual processes at the point of sale from inexperienced employees may mean errors or stress in cash acceptance (counterfeit handling and so on) and issuing of change. All of this may increase the visibility and exposure of cash, causing further risks, or at least perceived risks to store employees. In a manual environment, managing that risk may be done by employing more people, however the right Cash Automation solution can remove the responsibility (and stress) of cash handling from employees and includes automated validation, counting and secure storage of the cash.

Rising employee cost trends can also be countered with a Cash Automation strategy. So called “back office” solutions can supplement or replace administration and management staff, allowing them to focus more on the front of the store, customer service and so on. These administrative solutions can accept cash right at the point of sale, or in the back of the store, depending on the size and layout of the physical environment. They can dispense currency as well as accept, validate and secure the store’s revenue. Therefore, in addition to the reduction of cash administration staff costs, cash automation can assist with a broader self-service agenda and further remove front office employees away from checkouts and out onto the shop floor. In environments where checkouts remain, employers have added benefits of reassuring employees that cash need not be manually validated, counted or secured – the technology is there to do it all.

Finally, with rising interest rates being a key concern for retailers when considering access to capital for all their operation and initiatives, the right Cash Automation strategy coupled with a Cash Managed Service Provider can enable a retailer’s cash takings to work harder for them. In essence, providing faster access to that cash can make a huge difference to the retail operation, allowing payment of bills and financing of initiatives. Because the bank is aware of the counted cash for the day, and because the cash has been reliably deposited into a secure environment (which cannot be removed without approval), the bank can effectively transfer that cash to the retailer’s bank account while the balance physically remains in the retailer’s store. Costs of financing that balance (i.e., the interest charged for a “same day credit”) are likely to be significantly lower for the retailer than normal business lending rates – after all, the device is trusted, secure and the balance is counted automatically : the bank is assured of their cash !

Beyond these three areas, the benefits of Cash Automation can be even more interesting and expansive. For example, some retailers have experienced transformative safety-related improvements for their employees as they are able to “cash up” much earlier in the day. Other retailers have experienced reductions in store attacks, counterfeit attempts and so on because cash is “handled by technology” and not people.

What’s clear is that with pressures on business and consumers mounting, retailers must not leave any rock unturned in their search for operational improvements. Cash Automation becomes a more critical topic as consumers move back to a budgeting mechanism they can rely on to help them manage these economic headwinds.

At Cennox, we have a long and proven history of Cash Automation implementation. Our relationships with retailers are trusted and long lasting, and our experience is identifying areas of business benefits specific to a retailer’s needs, and building a solution to those needs is in our DNA. Through our technology, our services and our network of partners around the world, we offer Cash Managed Services to retailers and merchants of any size and in any sector.

We invite you to talk to us about your needs in Cash Automation, to share your thoughts on how these economic headwinds will affect your retail business, and to allow us to discuss with you how Cennox can help.

Written by:

Siôn Roberts

Group Chief Retail Officer at Cennox

LinkedIn | Twitter